Deposit growth dips below 8% in February

As of February 2025, total deposits in the banking system stood at Tk17,92,685 crore

Mousumi Islam, Dhaka

Published: 16 Apr 2025

Bangladesh’s banking sector is experiencing another slowdown in deposit growth, with the latest data showing the rate has fallen below 8%, intensifying concerns over liquidity and credit sustainability.

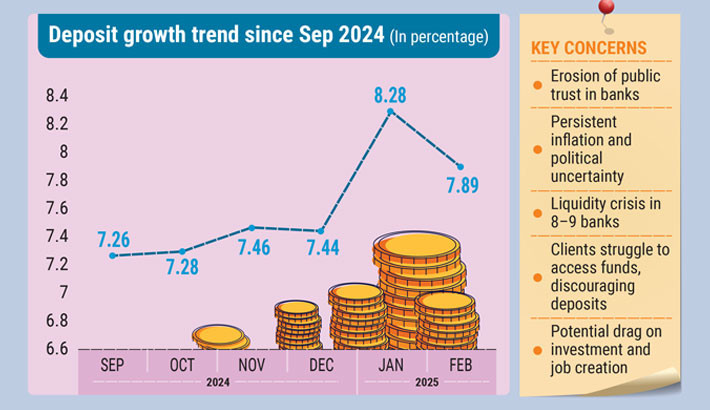

As of February 2025, total deposits in the banking system stood at Tk17,92,685 crore, up from Tk16,61,649 crore a year earlier—marking a year-on-year growth of 7.89%.

This is a decline from January’s 8.28% growth, which was the highest in four months.

Deposit growth has been on a downward trend since September, when it dipped to 7.26%, before marginally rising in the following months—7.28% in October, 7.46% in November, and 7.44% in December.

According to Bangladesh Bank data, time deposits account for 88% of total bank deposits. As of February, Tk1,90,303 crore was held in demand deposits, while the remaining Tk16,02,382 crore comprised time and other deposits.

Interest rates climb amid sluggish growth

In response to sluggish deposit mobilisation, banks are offering some of the highest interest rates in recent years—up to 12%—especially for short-term time deposits.

Private commercial banks currently offer an average interest rate of 9.68% on fixed deposits with tenures of less than one year, and 9.65% for those exceeding one year, including deposit pension schemes (DPS).

State-owned banks offer lower rates, averaging 8.90% for one-year deposits and 8.80% for longer terms.

Specialised banks offer around 7.95%, while foreign banks provide the lowest average rates—6.94% for under one-year deposits and 6.64% for longer tenures.

Experts cite confidence crisis

Economists attribute the slow deposit growth to persistent inflation, political instability, and an erosion of public trust in the banking sector.

Dr Zahid Hossain, former lead economist at the World Bank’s Dhaka office, told The Daily Sun that the decline is largely due to depositor anxiety, especially following cases where banks failed to return funds.

Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development and former chief economist of Bangladesh Bank, noted that 8–9 banks are currently facing liquidity crises.

“Clients at these banks struggle to access their funds, causing a drop in new deposits,” he said.

He warned that without stronger deposit growth, investment and job creation will stagnate, further weakening economic momentum despite slightly easing inflation.

Officials from several private banks, however, reported a notable increase in deposits in reputable institutions.

In contrast, customers are withdrawing from weaker banks, reflecting a broader shift in depositor behaviour driven by confidence and risk assessment.