Friday 26 April 2024

E-Paper

বাংলা

Previous Month

April 2024

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Su

Mo

Tu

We

Th

Fr

Sa

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

E-Paper

Newspaper

BN

Eid Magazine 2024

Photo Gallery

More News

AFD Group celebrates 10yrs of development partnership in Bangladesh

Bangladesh earmarks Tk385 billion for agriculture

PM seeks Chinese co-op for Bangladesh's southern region's dev

Bangabandhu was visionary of environment-friendly development: Saber

Govt following Green and Climate Resilience policy for environment-friendly dev: Saber

Hit by worker shortage, German city gets students to drive trams

Google Drive website finally gets dark mode

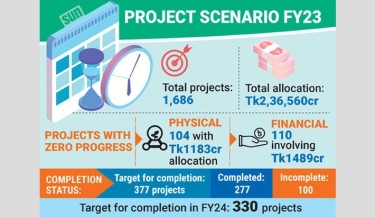

Projects grind to halt despite allocations

Trending

Better we prepare as another pandemic coming soon: Prof Nitish Debnath

Why Getting Visa Becomes a Wild Goose Chase!

17 die from heat stroke in 5 days

Father sentenced to death for raping daughter

SMART rate and inflation bite, businesses fight

‘Heat Alert’ extended for three more days

288 Myanmar security personnel sent back

Roasting Bangladesh: Tackling the Intense Heatwave

Say 'no' to wars: PM Hasina at UNESCAP meet

Usain Bolt named ambassador for T20 World Cup 2024

Xavi to remain Barcelona coach

Israel carrying out 'offensive action' in south Lebanon

Live Sports on TV Today

BNP serves showcause notice on 64 leaders

Vaccines saved at least 154 million lives in 50 years: WHO

Prayers for rain held at Baitul Mukarram

US sending senior officials to Niger to discuss troop exit

282 million people faced acute hunger in 2023, worst famine in Gaza: UN report

Bangladesh poised to exceed 1.01% global GDP share by 2028: IMF

Blinken calls for US, China to manage differences on charm offensive

Sajek road accident: Death toll rises to 9

Heatstroke kills 30 in Thailand this year as kingdom bakes

MPs can’t participate in campaigns: EC

GE HealthCare launches new refurbishing unit in Bangladesh

ACC writes to BFIU seeking wealth info of Benazir, his family members

3 new Appellate Division judges take oath

Malaria fight: Progress, but persists

FTII student’s film selected for Cannes’ La Cinef section

Nancy Pelosi calls for Netanyahu’s resignation

Rana Plaza victims demand fair compensation